August 24, 2025.

A review of the Letter to Shareholders for Q2, FY 2025, ended June 30, 2025, tells of the energetic progress Mercado Libre is making in its businesses.

Mercado Libre is focused on strengthening its competitive advantage of switching costs (value provided to existing customers that makes a switch to another provider uneconomic) and scale (the ability to utilize already existing capital to accomplish incremental sales, requiring relatively low incremental costs). It is doing so by continuing to advance three long term goals of the business, which mutually reinforce these competitive strengths. These goals are to provide the best value for advertisers in branding and search, build the Ecommerce platform of choice, and to become the largest fintech provider in Latin America.

E-commerce Logistics

Value provided to customers in shipping strengthens the switching costs for Mercado Libre’s e-commerce marketplace. Mercado Libre lowered the price threshold for free shipping from Brazilian Rial (R$) R$79 to R$19 (about US$3.5) (meaning the slower, free shipping is now available for items starting at R$19), and reduced shipping costs for sellers for items priced between R$79 and R$200). This lowers the friction to buyers and sellers of lower priced items. This is showing promising results with GMV accelerating in Brazil.

“We are committed to maintaining our competitive advantage in speed as we are convinced that fast delivery will always be in high demand. In fact, we still see solid demand for fast (paid) shipping on purchases below R$79 in Brazil despite the introduction of free (slower) shipping in this price range. “

It is harnessing it’s scale to continue reducing shipping costs and improve shipping times including for the slower free tier of shipping.

“Those opting for free shipping below R$79 are served with a slower, lower cost layer of our network that leverages existing infrastructure. We have operated this layer with limited volume for 18 months and are now scaling rapidly. Over time, we expect unit costs to fall and slow delivery promises to improve as we innovate, deploy technology and drive more volume through the network.

Mercado Libre is strengthening its competitive advantage over potential competitors. Competitors face the initial obstacle of shipping costs. Asian ecommerce companies like Temu, Shopee and AliExpress, already offered free shipping on the lower priced items, a segment where they have been stronger than Mercardo Libre. But Mercado Libre Mercado Libre has built the fastest shipping Network in Latin America. Its low shipping costs are possible because of its scale.

“Free shipping remains one of our most effective tools for bringing offline retail online and extending our position as Latin America’s largest ecommerce platform. For nearly a decade, we have offered free shipping on a large portion of our business, so we know it is a crucial driver of conversion, retention and customer satisfaction. “

Advertising

Mercado Libre’s advertising platform integrated with Google Ad Manager and AdMob. This integration expands it reach beyond Mercado Libre’s ecosystem. Advertisers can now seamlessly manage campaigns that simultaneously target consumers both inside and outside our ecosystem.

Fintech

The number of Mercado Pago monthly active users has doubled over the last two and a half years to reach almost 68 million MAUs in Q2’25, and engagement is growing as well. The relatively high yields on funds held in Mercado Pago savings accounts are key to attracting new users. This strategy has enabled Mercado Pago to build the largest retail money market fund in Argentina. In Brazil, there are about $180B in popular bank savings accounts which pay approximately 65% of benchmark rate, competing with Mercado Pago accounts which pay from 100% to 120% of the benchmark. With Mercado Pago’s competitive savings account yields, the nominal quarter over quarter increase in assets under management (AUM) in Brazil, Mexico and Chile in Q2’25 was the largest ever, with the total more than doubling YoY o $13.8B.

“Mercado Pago’s credit card performed strongly in Q2’25, with the portfolio growing 118% YoY to $4.0bn. The credit card was the primary driver of 91% YoY growth in the total credit portfolio in Q2’25. It now represents 43% of the$9.3bn book, up from 37% in Q2’24. In Brazil, the entire 2023 cohort is now NIMAL positive (NIMAL: Net Interest Margin After Losses), which is consistent with prior cohorts that typically reached this milestone within two years. ” Overall in the various countries the credit portfolio reflects satisfactory risk management.

In the offline Acquiring business, “We continued to gain market share across all major geographies in Q2’25 with Acquiring TPV growth of 53% YoY on an FX-neutral basis. “

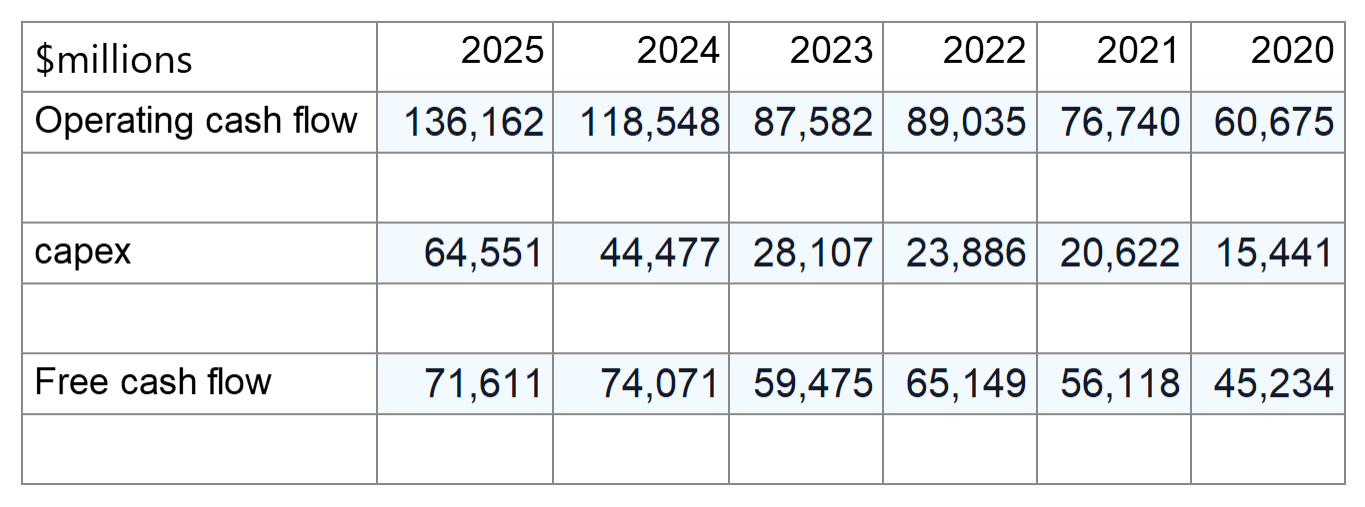

Consolidated Financial Results

Net income was negatively affected by a couple of factors.

There was a slight reduction in operating income margin due to added operating expenses from the extension of free shipping . Instead of taking the relevant revenue from providing shipping, the company is applying the incremental shipping costs as an operating expense to its gross profit. In Q2’25, income from operations grew 14% YoY to $825mn while the operating income margin contracted slightly by 2.10% yoy. The reduction in shipping charges was initiated in June, so we might expect further effects from this in the coming quarters.

But this expense is an investment that will result in stronger competitive advantage and increased engagement. Cheaper shipping drives increased engagement with ecommerce, thereby increasing revenue from linked services, including advertising, In the past, reduced shipping costs have been followed by gains in market share.

There was a non-operating expense, which is subtracted from operating income, which resulted in a lower net income. This was the Foreign Exchange (FX) losses of $117mn, which doubled YoY, mainly due to the devaluation of the Argentine Peso by 12% in April. As Mercado Libre sales in Argentina have grown, fluctuations in the Peso value will affect earnings accordingly. In 2023, there was a much larger devaluation of the Argentine peso by 50%. That year, FX losses for Mercado Libre were $239 million.

The Letter to Shareholders also noted that in July, Standard and Poors (S&P) upgraded Mercado Libre to investment grade with a rating of BBB-. Fitch had upgraded it to investment grade last year. Since its creation in 1999, Mercado Libre has been able to continue growing by successfully making investments in frontier markets, while also dealing with deterioration in the financial conditions, of one or another of the countries in which it operates. And that story of successful business decisions in the face of adversity is one of the things that makes Mercado Libre a remarkable company…